Rather than expanding the money supply, quantitative easing (QE) has actually caused it to shrink by sucking up the collateral needed by the shadow banking system to create credit. The “failure” of QE has prompted the Bank for International Settlements to urge the Fed to shirk its mandate to pursue full employment, but the sort of QE that could fulfill that mandate has not yet been tried.

Ben Bernanke’s May 29th speech signaling the beginning of the end of QE3 provoked a “taper tantrum” that wiped about $3 trillion from global equity markets – this from the mere suggestion that the Fed would moderate its pace of asset purchases, and that if the economy continues to improve, it might stop QE3 altogether by mid-2014. The Fed is currently buying $85 billion in US Treasuries and mortgage-backed securities per month.

The Fed Chairman then went into damage control mode, assuring investors that the central bank would “continue to implement highly accommodative monetary policy” (meaning interest rates would not change) and that tapering was contingent on conditions that look unlikely this year. The only thing now likely to be tapered in 2013 is the Fed’s growth forecast.

It is a neoliberal maxim that “the market is always right,” but as former World Bank chief economist Joseph Stiglitz demonstrated, the maxim only holds when the market has perfect information. The market may be misinformed about QE, what it achieves, and what harm it can do. Getting more purchasing power into the economy could work; but QE as currently practiced may be having the opposite effect.

Unintended Consequences

The popular perception is that QE stimulates the economy by increasing bank reserves, which increase the money supply through a multiplier effect. But as shown earlier here, QE is just an asset swap – assets for cash reserves that never leave bank balance sheets. As University of Chicago Professor John Cochrane put it in a May 23rd blog:

QE is just a huge open market operation. The Fed buys Treasury securities and issues bank reserves instead. Why does this do anything? Why isn’t this like trading some red M&Ms for some green M&Ms and expecting it to affect your weight? . . .

[W]e have $3 trillion or so [in] bank reserves. Bank reserves can only be used by banks, so they don’t do much good for the rest of us. While the reserves may not do much for the economy, the Treasuries they remove from it are in high demand.

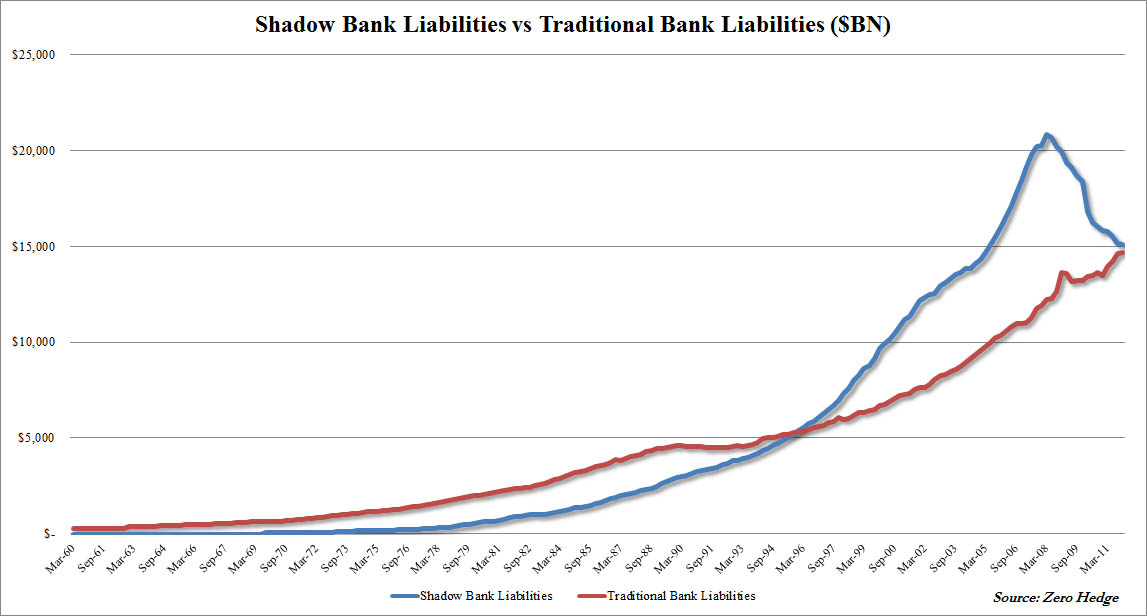

Cochrane discusses a May 23rd Wall Street Journal article by Andy Kessler titled “The Fed Squeezes the Shadow-Banking System,” in which Kessler argued that QE3 has backfired. Rather than stimulating the economy by expanding the money supply, it has contracted the money supply by removing the collateral needed by the shadow banking system. The shadow system creates about half the credit available to the economy but remains unregulated because it does not involve traditional bank deposits. It includes hedge funds, money market funds, structured investment vehicles, investment banks, and even commercial banks, to the extent that they engage in non-deposit-based credit creation.

Kessler wrote:

[T]he Federal Reserve’s policy—to stimulate lending and the economy by buying Treasurys—is creating a shortage of safe collateral, the very thing needed to create credit in the shadow banking system for the private economy. The quantitative easing policy appears self-defeating, perversely keeping economic growth slower and jobs scarcer.

That explains what he calls the great economic paradox of our time:

Despite the Federal Reserve’s vast, 4½-year program of quantitative easing, the economy is still weak, with unemployment still high and labor-force participation down. And with all the money pumped into the economy, why is there no runaway inflation? . . .

The explanation lies in the distortion that Federal Reserve policy has inflicted on something most Americans have never heard of: “repos,” or repurchase agreements, which are part of the equally mysterious but vital “shadow banking system.”

The way money and credit are created in the economy has changed over the past 30 years. Throw away your textbook.

Fractional Reserve Lending Without the Reserves

The post-textbook form of money creation to which Kessler refers was explained in a July 2012 article by IMF researcher Manmohan Singh titled “The (Other) Deleveraging: What Economists Need to Know About the Modern Money Creation Process.” He wrote:

In the simple textbook view, savers deposit their money with banks and banks make loans to investors . . . . The textbook view, however, is no longer a sufficient description of the credit creation process. A great deal of credit is created through so-called “collateral chains.”

We start from two principles: credit creation is money creation, and short-term credit is generally extended by private agents against collateral. Money creation and collateral are thus joined at the hip, so to speak. In the traditional money creation process, collateral consists of central bank reserves; in the modern private money creation process, collateral is in the eye of the beholder.

Like the reserves in conventional fractional reserve lending, collateral can be re-used (or rehypothecated) several times over. Singh gives the example of a US Treasury bond used by a hedge fund to get financing from Goldman Sachs. The same collateral is used by Goldman to pay Credit Suisse on a derivative position. Then Credit Suisse passes the US Treasury bond to a money market fund that will hold it for a short time or until maturity.

Singh states that at the end of 2007, about $3.4 trillion in “primary source” collateral was turned into about $10 trillion in pledged collateral – a multiplier of about three. By comparison, the US M2 money supply (the credit-money created by banks via fractional reserve lending) was only about $7 trillion in 2007. Thus credit-creation-via-collateral-chains is a major source of credit in today’s financial system.

Exiting Without Panicking the Markets

The shadow banking system is controversial. It funds derivatives and other speculative ventures that may harm the real, producing economy or put it at greater risk. But the shadow system is also a source of credit for many businesses that would otherwise be priced out of the credit market, and for such things as credit cards that we have come to rely on. And whether we approve of the shadow system or not, depriving it of collateral could create mayhem in the markets. According to the Treasury Borrowing Advisory Committee of the Securities and Financial Markets Association, the shadow system could be short as much as $11.2 trillion in collateral under stressed market conditions. That means that if every collateral claimant tried to grab its collateral in a Lehman-like run, the whole fragile Ponzi scheme could collapse.

That alone is reason for the Fed to prevent “taper tantrums” and keep the market pacified. But the Fed is under pressure from the Swiss-based Bank for International Settlements, which has been admonishing central banks to back off from their asset-buying ventures.

An Excuse to Abandon the Fed’s Mandate of Full Employment?

The BIS said in its annual report in June:

Six years have passed since the eruption of the global financial crisis, yet robust, self-sustaining, well balanced growth still eludes the global economy. . . .

Central banks cannot do more without compounding the risks they have already created. . . . [They must] encourage needed adjustments rather than retard them with near-zero interest rates and purchases of ever-larger quantities of government securities. . . .

Delivering further extraordinary monetary stimulus is becoming increasingly perilous, as the balance between its benefits and costs is shifting.

Monetary stimulus alone cannot provide the answer because the roots of the problem are not monetary. Hence, central banks must manage a return to their stabilization role, allowing others to do the hard but essential work of adjustment.

For “adjustment,” read “structural adjustment” – imposing austerity measures on the people in order to balance federal budgets and pay off national debts. The Fed has a dual mandate to achieve full employment and price stability. QE was supposed to encourage employment by getting money into the economy, stimulating demand and productivity. But that approach is now to be abandoned, because “the roots of the problem are not monetary.”

So concludes the BIS, but the failure may not be in the theory but the execution of QE. Businesses still need demand before they can hire, which means they need customers with money to spend. QE has not gotten new money into the real economy but has trapped it on bank balance sheets. A true Bernanke-style helicopter drop, raining money down on the people, has not yet been tried.

How Monetary Policy Could Stimulate Employment

The Fed could avoid collateral damage to the shadow banking system without curtailing its quantitative easing program by taking the novel approach of directing its QE fire hose into the real market.

One possibility would be to buy up $1 trillion in student debt and refinance it at 0.75%, the interest rate the Fed gives to banks. A proposal along those lines is Elizabeth Warren’s student loan bill, which has received a groundswell of support including from many colleges and universities.

Another alternative might be to make loans to state and local governments at 0.75%, something that might have prevented the recent bankruptcy of Detroit, once the nation’s fourth-largest city. Yet another alternative might be to pour QE money into an infrastructure bank that funds New Deal-style rebuilding.

The Federal Reserve Act might have to be modified, but what Congress has wrought it can change. The possibilities are limited only by the imaginations and courage of our congressional representatives.

______________________

Ellen Brown is an attorney, president of the Public Banking Institute, and author of twelve books including Web of Debt and its recently-published sequel The Public Bank Solution. Her websites are http://WebofDebt.com, http://PublicBankSolution.com, and http://PublicBankingInstitute.org.

Filed under: Ellen Brown Articles/Commentary |

Excellent, Ellen; thank you! The goal from the Fed of full-employment is an Orwellian lie. You’re right that it could be done if government became employer of last resort for infrastructure investment.

The benefits of such a policy:

1. Full-employment.

2. The best infrastructure (hard and soft) we can imagine.

3. No debt or cost when financed with debt-free money, and actual falling overall prices because infrastructure returns more economic output than costs.

What we have is economic “leadership” engaged in obvious fraud: intentional deception with trillions in damages from those with fiduciary responsibility to represent public interests.

This performance of centralized power is powerful evidence for more localized and accountable public banks.

Righton, Carl. And Ellen’s new book, The Public Bank Solution, shows that it works.

It’s past time to stop the monetary talk and begin the law enforcement talk. Enough of us know all we need to know to do what we must do to save our civilization from the subhumans in monetary clothes, and talking ourselves to death in ivory towers just lets them buy time to orchestrate their usual catastrophic diversions. The subhumans have been committing massive crimes against humanity for centuries. If government officials are too corrupt to enforce the laws of their countries, then those officials’ delegated authority has reverted to the citizens who must now exercise their God-given right of self-defense. It is our right and duty to “throw off” despots, be they political or monetary. Saddle up, or clean the stables. .

Public banking authorized to lend legal tender that would protect states and municipalities from current interest burdens (and impose lesser rates of interest and/or zero rates for very long periods of time) sounds like a good idea. To create such authorization will take an act of Congress or an executive order by the president in time of war or emergency as serious as war. I would favor such a concept or authority when and if declared.

I would also favor such lending to customers of public banks, if the above authority were ever enacted or declared.

Pending such enchantment or presidential order, Quantitative Easing does a similar job if Congress or the president pushes hard on the investment/spending pedal to rescue the middle class and the nation itself from its self-imposed contraction.

All money is based on output for sale. We all know it. But we, the people, have not followed our knowledge to its necessary conclusions.

The way I see it is that the financial sector is a conglomerate of inter locking ponzi schemes and the markets for all major commodities ,right down to chocolate it seems, are price fixed, with little co-relation to supply or demand. At the very beginning of the QE’s I posted the common knowledge that these measures would be tantamount to pushing on a string.

The financial sector, since they blew up the economy in 2008, has been looking for an overall solution that totally lays within their balliwick all the while trying to keep the game going and the profits coming in. As we all know the solution does not dwell within monetary gesturing but with government fiscal engineering.The bankers blew up the economy and themselves only to find all the debt they had buried their customers in has killed the productive side. Now they’re scared and want all that’s owed to them. In the meantime these compulsive gamblers have been creating and playing all kinds of new games with derivatives etcetera. Any number of scenarios could start toppling the dominoes and finish this go around, the last was the Great Depression. As it is we now have a slow rolling depression/recession as far as the eye can see as no one has enough left to be able to afford much more bankers money.The poor parasitic Fed, their captive host that they have been sucking blood out of for 100 years, well they’ve just about sucked it dry and killed their food source.

Does anyone subscribe to the theory that the Fed cannot raise interest rates while the public debt is so high, unless they want to bankrupt themselves?

The Fed can’t do everything that is needed. Congress needs to

abandon faulty monetary theories which treat federal finances as

like state or local government finances, or household, or business

finances–all of which have to get their money from elsewhere to spend or pay off debts. The federal government looks like it is

borrowing money when it sells Treasury securities, but any debts

it creates by borrowing from banks, get paid off by newly created

money from the Fed when it buys the securities from the banks.

Congress sets in motion the creation and introduction of new money

into circulation by the Fed when Congress deficit spends. Treasury sells securities to banks to cover the deficit. Then at some later point when the securities mature, it buys them from the banks. That redeems the debt. The Fed is not owed more than a relatively

small transaction fee to cover it operations: 6% of the interest on the securities.

So Congress needs to deficit spend big time to get us out of this

recession and slump.

But Ellen has some good ideas such as suggesting the Fed can

buy up all those student loans and reissue them at 0.75% interest.

But Congress could similarly create such loans, or even guarantee

everyone a university education if they are capable of it, debt-free.

That went completely over my head I’m afraid. Can you translate that to English please ?!

[…] Ellen Brown Writer, Dandelion Salad webofdebt.com July 23, […]

“The possibilities are limited only by the imaginations and courage of our congressional representatives.”

Enough said..

Congress should start to clean up the debt by repealing the law they passed that is bankrupting the post office that requires prepayment into the retirement account.

Isn’t it simply just a case of the banks directing loans to the things that will make it the most profits such as putting it in stocks and shares to raise the value of asset and into derivatives rather than directing the money banked against the government created reserves going into the real economy where it is actually supposed to be going and where it is going to do the most good?

All that has to be done is to force the banks to direct the money into the real economy, surely?

Or is that simplifying things too much?

Why banksters laugh with the recent ECOFIN decision

http://failedevolution.blogspot.gr/2013/07/why-banksters-laugh-with-recent-ecofins.html

[…] Ellen Brown Web of Debt […]

[…] Read More […]

Reblogged this on wchildblog.

[…] READ MORE HERE […]

This is an excellent observation, that the current version of QE merely swaps assets and slightly overpays for them. The aid to banks’ balance sheets is mostly to the extent that the purchased assets are bid up by the Fed. This “overpayment” subsidy is small as a proportion of QE. Yet the shortage of collateral being created, multiplied by 3x into shadow banking credit, is far greater than the boos of this overpayment.

Meanwhile, major banks are not creating much credit to the real economy.

The Treasury and Congress can easily cut income taxes by a major amount (perhaps not interest income), in this way sending QE to those who are income-generating. It can eliminate income taxes altogether, or give an income tax credit as an incentive.

This credit could be for individuals and businesses for non-investment incomes of up to $500,000, excluding any investment and interest income from the basis for the tax credit.

Profitable businesses would look to scale up operations.

Another option is to give banks a 2% interest credit for any loans made for productive purposes that do not default. Loans that default, or that go to real estate, would not count. This would incentivize banks to lend to the real economy, rather than to real estate and to the federal government. Soon enough, banks would not only increase loans, but also renegotiate existing loans – calling them in and offering, say, a 1% discount under the same terms.

Elizabeth Warren’s idea is great, but students are a small portion of the population, and in any case the result may well be even higher tuitions!

Whatever form QE takes, it must consider a stop to buying new Treasuries and in this way sucking up base collateral for the shadow banking system.

[…] Collateral Damage: QE3 and the Shadow Banking System […]

[…] Collateral Damage: QE3 and the Shadow Banking System (webofdebt.wordpress.com) […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]

[…] to avoid the appearance of impropriety by borrowing from the repo market. (See my earlier article here.) The banks’ excess deposits are first used to purchase Treasury bonds, agency securities, and […]