Rather than making money harder to get, the U.S. government needs to focus on the other side of the demand vs. supply equation.

In prescribing cures for inflation, economists rely on the diagnosis of Nobel laureate Milton Friedman: inflation is always and everywhere a monetary phenomenon—too much money chasing too few goods. But that equation has three variables: too much money (“demand”) chasing (the “velocity” of spending) too few goods (“supply”). And “orthodox” economists, from Lawrence Summers to the Federal Reserve, seem to be focusing only on the “demand” variable.

The Fed’s prescription is to suppress demand (borrowing and spending) by raising interest rates. Summers, a former U.S. Treasury Secretary who presided over the massive post-2008 bank bailouts, is proposing to reduce demand by raising taxes or raising unemployment rates, reducing disposable income and thus people’s ability to spend. But those rather brutal solutions miss the real problem, just as Summers missed the crisis leading up to the 2008-09 crash. As explained in a November 2021 editorial titled “Too Few Goods – The Simple Explanation for October’s Elevated Inflation Rates,” we don’t actually have too much consumer money chasing available goods:

M2 money supply surged [in 2020] as the Fed pumped out liquidity to replace businesses’ lost sales and households’ lost paychecks. But bank reserves account for nearly half of the cumulative increase since 2020 began, and the vast majority seem to be excess reserves sitting on deposit at Federal Reserve banks and not backing loans. Excluding bank reserves, M2 money supply is now growing more slowly than it did for most of 2015 – 2019, when inflation was mostly below the Fed’s 2% y/y target, much to policymakers’ chagrin. Weak lending also suggests money isn’t doing much “chasing,” a notion underscored by the historically low velocity of money. US personal consumption expenditures—the broadest measure of household spending—have already slowed from a reopening resurgence to rates more akin to the pre-pandemic norm and surveys show many households used stimulus money to repay debt or build savings they may not spend at all. It doesn’t look like there is a mountain of household liquidity waiting to do more chasing from here. [Emphasis added.]

In March 2022, the Federal Reserve tackled inflation with its traditional tools – raising interest rates and tightening the money supply by selling bonds, pulling dollars out of the economy. But not only have prices not gone down since then, they are going up. As observed in a July 15 article on Seeking Alpha titled “Fed-Induced Recession Looms As Rate Fears Roil All Markets”:

On Wednesday, the Consumer Price Index came in at a 9.1% annual rate. The higher-than-expected reading puts the CPI at a new 41-year high.

The biggest contributors to rising consumer prices are the basic necessities of food, fuel, and shelter. As households struggle to make ends meet, they are trimming discretionary spending, burning through savings, and running up credit card balances.

Businesses are also getting squeezed. On Thursday, the Producer Price Index showed wholesale costs rising at a massive 11.3% year-over-year.

When their own costs go up, producers must raise the prices of their products to cover those costs, regardless of demand. Less money competing for their products won’t bring producer costs down. It will just drive the companies out of business, as happened in the Great Depression. The Seeking Alpha article concludes:

… As both businesses and consumers are forced to tighten their belts, a slowdown looms.

And if the Federal Reserve makes another major policy misstep, then a severe recession and financial crisis may also be coming.

Recession is already evident. The stock market has lost a cumulative $7 trillion in value this year, while the crypto market has lost $2 trillion since last November. Emerging markets are in even worse straits. According to a July 14 article by Larry McDonald on ZeroHedge, “Emerging and frontier market countries currently owe the IMF over $100 billion. US central banking policy plus a strong USD is vaporizing this capital as we speak.… A quarter-trillion dollars of distressed debt is threatening to drag the developing world into a historic cascade of defaults.”

Every time the Fed raises rates, borrowing becomes more expensive. That means higher interest costs not only for governments but for borrowers with mortgages, home equity lines of credit, credit cards, student debt and car loans. For both large and small businesses, loans also get pricier.

To be clear, this is not the same sort of inflation that Paul Volcker was taming in 1980 when he raised the Fed funds rate to 20%. McDonald observes, “In 2021, global debt reached a record $303T, according to the Institute of International Finance .… Volcker was jacking rates into a planet with about $200T LESS debt.” [Emphasis added]

Volcker was also not dealing with the supply shortages we have today, generated by lockdowns that put more than 100,000 U.S. companies out of business; sanctions and war that cut off global supplies of fuel, food and resources; and farming crises such as that in the Netherlands, generated by overly stringent regulations.

Higher interest rates don’t alleviate cost/push inflation caused by supply crises; they make it worse. Rather than making money harder to get, the government needs to focus on the supply side of the equation, stimulating local production to bring supply levels up. Rather than Volcker’s solution, what we need is that pioneered by Alexander Hamilton, Abraham Lincoln, and Franklin D. Roosevelt, who pulled us out of similar crises with public banking institutions designed to stimulate infrastructure and development.

For foreign models, we can look to the infrastructure-funding central banks of Australia, New Zealand and Canada in the first half of the 20th century; and to China, which salvaged the global economy following the 2008 banking crisis with massive infrastructure and development funded through its state-owned development banks.

China Did It

In the last 40 years, China has exploded from one of the world’s poorest countries to a global economic powerhouse. Among other notable achievements, from 2008 to 2022 it built 23,500 miles of high-speed rail, at a time when U.S. infrastructure projects were stalled for lack of funding. How did China pull this off? Rather than relying on taxpayer funds or foreign debt, it borrowed from its own banks.

China has three massive state-owned infrastructure and development banks – the China Development Bank, the Export-Import Bank of China, and the Agricultural Development Bank of China. Called “policy banks,” they get their liquidity either (a) directly from the People’s Bank of China (PBOC) in the form of “Pledged Supplementary Lending,” or (b) by issuing bonds, which have higher credit ratings than commercial bank bonds and are in demand because they can be used as collateral to borrow from the central bank. China’s policy banks are limited to funding certain specific government policies; and these policies are all productive and public-purpose-driven, unlike the short-term private profit-maximization driving Wall Street banks.

Besides its big state-owned banks, China has an extensive network of local banks, which know their local markets. The PBOC website lists seven tools it can use for adjusting monetary policy, including not just a short-term lending facility like the U.S. Fed’s discount window, but a facility to inject liquidity into banks for medium-term loans, as well as the “pledged supplementary lending” to fund long-term loans from the three policy lenders for specific sectors, including agriculture, small businesses, and shanty town re-development.

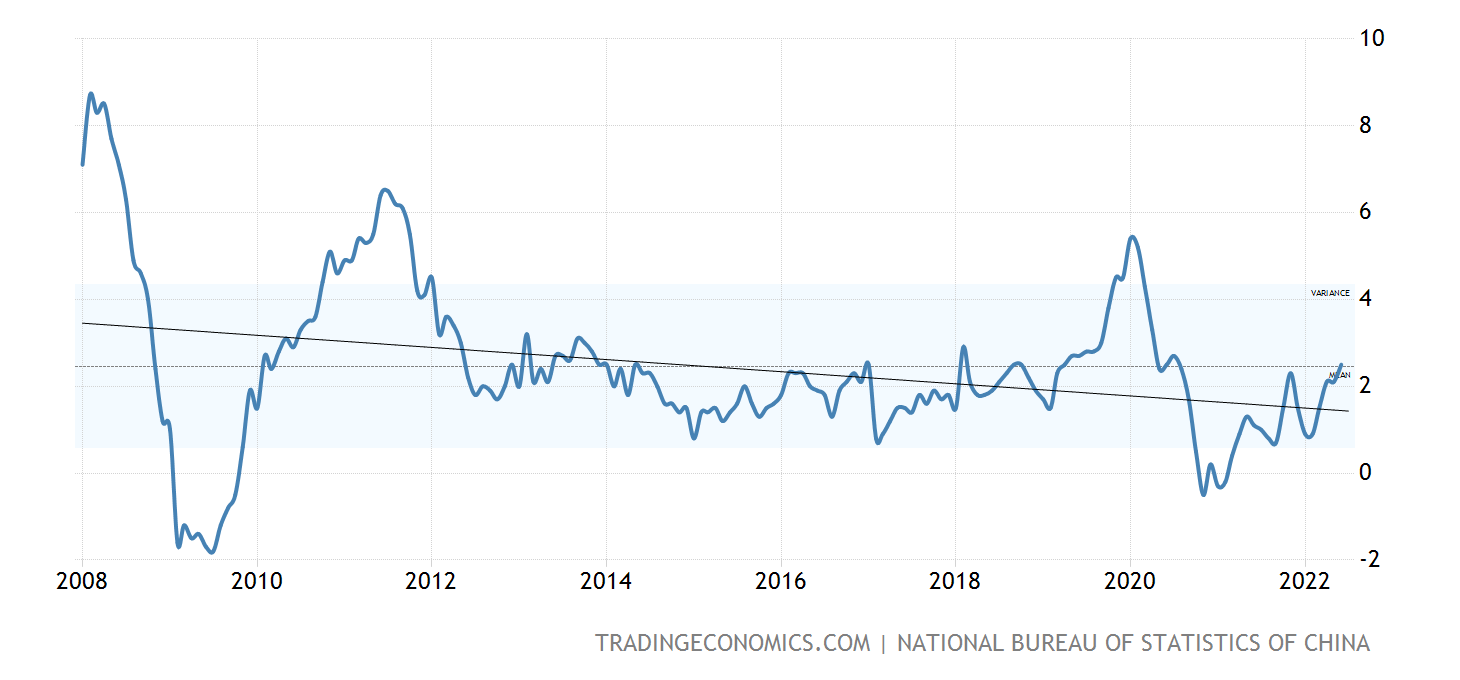

Yet all this stimulus has not driven up Chinese prices. In fact consumer prices initially fell in 2008 and have hovered around 2% ever since. [See chart below.]

Prices are creeping up now, as is happening everywhere; but they have reached only 2.5%—far below the 9.7% seen in the U.S. in July.

Our Forebears Did It Too

State-owned infrastructure banks are not unique to China. In the United States, a similar model was initiated by Alexander Hamilton, the first U.S. Treasury Secretary. The “American System” of government-issued money and credit was key both to winning the American Revolutionary War and to transforming the nation from a collection of agrarian colonies to an industrial powerhouse. But after the War, the federal government was $70 million in debt, including $44 million from the colonies-turned-states.

Hamilton solved the debt problem with debt-for-equity swaps. Debt instruments were accepted in partial payment for stock in the First U.S. Bank. This capital was then leveraged into credit, issued as the first U.S. currency. Loans were based on the fractional reserve model. Hamilton wrote, “It is a well established fact, that Banks in good credit can circulate a far greater sum than the actual quantum of their capital in Gold & Silver.”

That was also the model of the Bank of England, the financial engine of the colonial oppressors; but there were fundamental differences between the two models. The Bank of the United States (BUS) was designed for public development. The Bank of England (BOE) was intended for private gain. (See Hamilton Versus Wall Street: The Core Principles of the American System of Economics by Nancy Spannaus, and Alexander Hamilton: A Biography by Forrest McDonald.)

The BOE was chartered to fund a national war and was capitalized exclusively by public debt. The government would pay private lenders, who controlled what policies could be funded. Hamilton’s BUS, by contrast, was to be a commercial bank, funding itself by generating credit for infrastructure and development.

Under Hamilton’s system of “Public Credit,” the primary function of the BUS would be to issue credit to the government and private interests for internal improvements and other economic development. Hamilton said a bank’s function was to generate active capital for agriculture and manufactures, increasing the quantity and quality of labor and industry. The BUS would establish a sovereign currency, a banking system, and a source of credit to build the nation, creating productive wealth, not just financial profit.

The BUS was chartered for only 20 years, after which it lapsed. When economic hardships and monetary pressures followed, the Second Bank of the United States was founded in 1816 under President John Quincy Adams, basically on the Hamiltonian model. It funded one of the most intense periods of economic progress in history, investing directly in canals, railroads, roads, and coal and iron enterprises; lending money to states and cities engaged in such projects; and managing credit so that it continually flowed into needed productive activities.

After the Second BUS was shut down, Abraham Lincoln’s government issued Greenbacks (U.S. Notes) directly, funding both the Civil War and extensive infrastructure and development. The National Banking System was also established, under which national banks would be partially capitalized with federal securities.

An International Movement Is Born

The American System and its leaders not only allowed the American colonists to break free of British control but inspired an international movement. Other British colonies revolted, including Australia, New Zealand and Canada; and other countries rebelled against the British imperial free-trade doctrines and developed their own infrastructure and manufacturing, including Germany, Ireland, Russia, Japan, India, Mexico, and South America.

The Commonwealth Bank of Australia (CBA), founded in 1911, followed the Hamiltonian model. It was masterminded by an American named King O’Malley, who called Hamilton “the greatest financial man who ever walked the earth.” The CBA funded major national development and Australia’s participation in World War I, simply with national credit issued by the bank.

In Canada from 1939-74, the government borrowed from its own Bank of Canada, effectively interest-free. Major government projects were funded without increasing the national debt, including aircraft production during and after World War II, education benefits for returning soldiers, family allowances, old age pensions, the Trans-Canada Highway, the St. Lawrence Seaway project, and universal health care for all Canadians.

Meanwhile in the U.S., we got the Federal Reserve – and the worst banking crisis and economic depression ever in 1929-33. Pres. Franklin D. Roosevelt then rebuilt the U.S. economy financed through the Reconstruction Finance Corporation, again funded on the Hamiltonian model. Initially capitalized with $500 million, from 1932 to 1957 it lent or invested over $40 billion for infrastructure and development of all kinds; funded the New Deal and World War II; and turned a net profit to the government of $690 million.

Solving Today’s Price Inflation

That could be done again, assuming the political will. Some pundits predict that the Fed will back off its aggressive interest rate hikes when the carnage from that approach becomes painfully evident, but it seems to be a phase we have to go through to convince policymakers that the Fed’s current tools are not able to curb the price inflation we have today. We need to stimulate local development with a national infrastructure and development bank like China’s; and for that, Congress needs to pass an infrastructure bank bill.

Four such bills are currently before Congress. Only one, however, is capable of generating the nearly $6 trillion that the American Society of Civil Engineers says is needed over the next decade for U.S. infrastructure investment. This is HR 3339: The National Infrastructure Bank Act of 2021, which would effectively be self-funded on the American System model – a critical feature given that the federal debt is at record levels. The bank would be capitalized with federal debt acquired in debt-for-equity swaps – federal securities for non-voting bank shares paying a 2% dividend. This capital would then be leveraged at 10 to 1 into low-interest loans, essentially at cost. The bank would be anti-inflationary, by bringing supply up to meet demand; would not require new taxes but would rather increase the tax base, by increasing GDP; and would require only a small Congressional outlay for startup costs, which would quickly be repaid. For more information on HR 3339, see the National Infrastructure Bank Coalition website.

_______________________

This article was first posted on ScheerPost. Ellen Brown is an attorney, chair of the Public Banking Institute, and author of thirteen books including Web of Debt, The Public Bank Solution, and Banking on the People: Democratizing Money in the Digital Age. She also co-hosts a radio program on PRN.FM called “It’s Our Money.” Her 300+ blog articles are posted at EllenBrown.com.

Filed under: Ellen Brown Articles/Commentary | Tagged: 2022 INFLATION, Ellen Brown, FED INFLATION, Inflation, interest rates, LAWRENCE SUMMERS, Lockdown, Paul Volcker, public banking, US INFLATION |

It’s not the US government that needs to focus on the need for more liquidity but the free market. Only the free market can legally and efficiently monetize debt-free medium derived from precious metal and safely have that medium (market currency) entered into circulation.

The monetary model is not flawed. It’s simply incomplete much like a bicycle designed for two wheels with only one wheel assembled onto the frame. Would you expect to crash ???

Reading Ellen’s article again and reading through these comments, it occurs to me , an admitted novice, that most of the “fixes” are on the level of the problem. Let’s TRANSCEND the problems and go back to before the fraudulently named Bank of North America DEBT NOTES , to the original SOVEREIGN MONEY – the Continental Currency – with which America was kicking the ass of arguably the greatest super power of the time – England – and doing it debt and usury free.

The main purpose of the war for the Brits (or rather the “Bank of England” in the “City of London” – nod nod, wink wink) was to STOP that currency. British General Howe with New Amsterdam / New York City Tory Loyalists. tried to destroy the Continentals with massive counterfeiting.

Printing presses on Brit gunships in NY harbor cranked out an estimated BILLION when the Continental Congress had only authorized and printed $250 mm. The fake currency was advertised in NY papers as “easy to get off” and sold in tea shops and restaurants for the cost of the paper.

All the Continentals over a dollar WERE “backed” by gold or silver, btw – which proved to be a major part of their destruction, as the bastard Hamilton BRIBED the State and Commonwealth representatives to the convention in Philadelphia “TO IMPROVE THE ARTICLES OF CONFEDERATION,” to close the shutters and lock the doors, and declare a CONstitutional CONvention.

He promised that if they would write a new “federal” constitution to destroy the States’ Sovereign MONEY POWER and concentrate all such power in CONgress (with a loophole large enough to drive through three PRIVATE central banks masquerading as public / government,) that he would redeem their “worthless” Continentals at face value.

Lo and behold, the very first act of the new CONgress, with fox Hamilton as secretary in the treasury henhouse, was the 20 year charter of the -wait for it – First Bank of the United States.

[An interesting aside if I may: silversmith, engraver, and midnight rider Paul Revere, carved some of the printing press ink blocks for the REAL Continentals.]

Henry Ford and Thomas Edison had the “FED” scam sussed soon after it was created. Why they asked, rhetorically, do we let banks create money out of thin air on OUR credit – “the full faith and credit of the US government” – and LOAN it to us at interest, when WE (America) can do the same, free of debt and usury?

Sovereign Money is fundamental to the Affluence and Peace in a New Invincible America. The solution to the current and ALL inflation is to take back the MONEY POWER as President Van Buren wrote it in all caps, and issue TRUE fiat money – Sovereign currency free of debt and usury.

The economic engine is being run in reverse. It’s simple. Lending by the banks is inflationary (increases the volume and turnover of new money). Lending by the nonbanks is noninflationary (results in the turnover of existing money). The fallacious Gurley-Shaw thesis has run its course.

In 2010, the PBOC’s RRR went to 18.5% – “to sterilize over-liquidity and get the money supply under control in order to prevent inflation or over-heating”

If you wanted to get rid of inflation, you should stop expanding the money supply, indeed drain the money stock, and then gradually drive the banks out of the savings business (increasing velocity).

The 1966 Interest Rate Adjustment Act is prima facie evidence. M1 peaked @137.2 on 1/1/1966 and didn’t exceed that # until 9/1/1967. Deposit rates of banks decreased from a high range of 5 1/2 to a low range of 4 % (albeit not enough). A .75% interest rate differential was given to the nonbanks.

A recession, as Powell claimed (“Powell cited 1965, 1984 and 1994 as examples where the FED corrected the economy without a recession.”), was avoided.

The “taper tantrum” represents the activation of monetary savings (where S = I), where the FDIC reduced deposit insurance from unlimited transaction deposits to $250,000.

QE3 didn’t expand the volume of money (inflationary) as much as it increased the velocity (noninflationary) of circulation. Monetary flows, the volume and velocity of money actually fell by 80 percent causing the price of oil to trough in Jan 2016 by 70 percent during the same period.

It had a number of positive effects, a dramatic rise in the real rate of interest for saver-holders, R *, a drop in inflation, and an accelerated drop in the unemployment rate from 8.0% to 5.0% by Dec. 2015.

Yet Janel Yellen, presumably looking at U *, decided to raise policy rates too early on 12/17/2015 from .25 to .50%.

People are ignorant. They don’t know what just happened. Powell eliminated legal reserves but didn’t at the same time increase capital requirements (as all the other Central Banks did who eliminated RRs).

Brilliant as always, Ellen, but THE core problem remains: money is debt and the interest – the vig – doesn’t exist. The uncreated interest is the crucial problem and why the crooked PRIVATE (((“enterprise”))) is CRASHING and being exposed.

As you know I do not share your praise of Hamilton. I consider him a traitor and mole, and the real father of the CONstitutiin – THE primary purpose of which was to regain (((their))) central bank after his and Robert Morris’ Bank of North America – which eliminated the GLORIOUS Continental Curreny – was torpedoed.

https://fairfieldjournal.org/things-i-know-about-money-p475-287.htm

As usual, a great explanation of what is and what should be our method of putting money into circulation. Thank you

The problem is that the FED’s Ph.Ds. in economics don’t know money from liquid assets. Banks are not intermediaries.

Take the Depository Institutions Deregulation and Monetary Control Act of 1980 history.

Depository Institutions Deregulation and Monetary Control Act of 1980 | Federal Reserve History

It says: “So, banks and other traditional types of depository institutions were at a severe disadvantage in attracting deposits compared with less-regulated competitors, such as money market mutual funds.”

And: “Other depository institutions, such as savings and loans and credit unions, whose deposits are also part of the money supply, were not subject to the Fed’s reserve requirements.”

Neither is true. Both the MMMFs and “other depository institutions” are customers of the DFIs.

This stood out for me about Ellen’s quote on the CPI: The biggest contributors to rising consumer prices are the basic necessities of food, fuel, and shelter. As households struggle to make ends meet, they are trimming discretionary spending, burning through savings, and running up credit card balances.

Ummm – food, shelter, fuel are all land and natural resource based. Funny how the Law of Rent plays out (land values rise faster than wages) in the exploitation of both “consumers” and “producers.” The fox in the henhouse is the Land Problem, a predominant concern of classical economics, conveniently ignored by neoliberal economics after this field of inquiry was thoroughly corrupted. Combined with Ellen’s push for public banks, let’s support tax shift away from wages and production and onto land and resources (commons rent public finance). For more see. http://www.theIU.org

Also note that while China has its state bank which is great, it also has the problem of land price and thus housing inflation.

[…] Interest Rate Hikes Will Not Save Us from Inflation, by Ellen Brown […]

[…] Original Post […]

[…] source ellenbrown.com | Ellen Brown | […]

[…] Interest Rate Hikes Will Not Save Us from Inflation | WEB OF DEBT BLOG […]

Link: “HOUSING IS THE BUSINESS CYCLE” Edward E. Leamer

Click to access w13428.pdf

Problem is, like the GFC, a deceleration in new residential housing exacerbates the existing housing shortage. So existing sale prices are given new support.

“Even before the pandemic, in 2019, the U.S. was short 3.8 million homes — both places to rent and places to own”.

The economy is being run in reverse. Lending/investing by the Reserve and commercial banks is inflationary (increases the volume and turnover of new money). Whereas lending/investing by the nonbanks is noninflationary, other things equal (results in the activation of existing money).

The 1966 Interest Rate Adjustment Act is prima facie evidence.

Great post. The economy needs debt-free liquidity that the free market is working hard at as we speak.

The economy is being run in reverse, banks are not intermediaries. But Powell eliminated reserve requirements against commercial bank deposit liabilities. And the last vestige of legal reserve and reserve ratio requirements against the Federal Reserve Note, demand deposit, and inter-banks demand deposit liabilities of the Reserve banks was eliminated in 1968. Today the Federal Reserve Note has no legal reserve requirements, and the capacity of the Fed to create IBDDs has no legal limit. These IBDDs are owned by commercial banks; they are bank free-gratis legal reserves and can be converted dollar-for-dollar into Federal Reserve Notes. The volume of IBDDs is almost exclusively related to the volume of Reserve Bank credit. When Federal Reserve Banks expand credit, for example by buying U.S. obligations, the balance sheets of the Banks reflect an increase in earning assets and an equal increase in IBDD liabilities, i.e., free-gratis legal reserves (not a tax).

[…] https://ellenbrown.com/2022/07/28/interest-rate-hikes-will-not-save-us-from-inflation/ […]

[…] 500 slumping almost 20%, as the Federal Reserve battled soaring inflation with aggressive interest rate hikes that roiled […]