On January 30, when former Federal Reserve board member Kevin Warsh was nominated by President Trump as the central bank’s next chair, markets sold off and gold and silver plunged. Investors were positioned for a “dove,” someone inclined to cut rates aggressively and keep money loose; and Warsh has a long-standing reputation as a “hawk.”

So wrote Michael Nicoletos in an article titled “Everyone Is Focusing on the Wrong Thing.” But Nicoletos and some other commentators are seeing something else on the horizon – a rebalancing of the banking system through an overhaul of the Federal Reserve itself. In recent months, noted Nicoletos, Warsh has argued that the central bank’s “bloated balance sheet” has made borrowing “too easy” for Wall Street, while leaving “credit on Main Street too tight.” That contrast — abundant liquidity for the largest financial institutions, scarcity for the communities that actually generate economic activity — is a structural flaw that has unbalanced the American economy.

Albert Einstein is often quoted as saying that compound interest is “the most powerful force in the universe.” The quote is probably apocryphal, but it reflects a mathematical truth. Interest on earlier interest grows exponentially, outrunning the linear growth of revenue and eventually consuming everything.

That is where the United States now stands. The government does pay the interest on its debt every year, but it is having to pay it with borrowed money. The interest curve is rising exponentially, while the tax base is not.

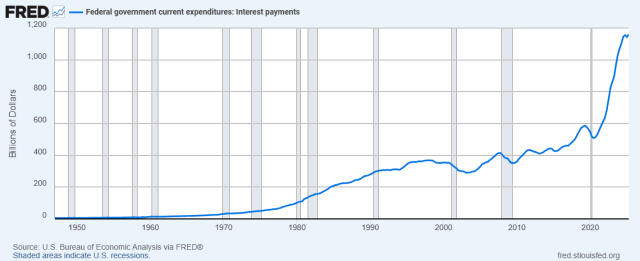

Interest is now the fastest growing line item in the entire federal budget. The government paid $970 billion in net interest in FY2025, more than the Pentagon budget and rapidly closing in on Social Security. It already exceeds spending on Medicare and national defense and is second only to Social Security. The Congressional Budget Office projects that interest will reach nearly $1.8 trillion by 2035 and will cost taxpayers $13.8 trillion over the next decade. That is roughly what Social Security will pay out over the same decade (about $1.6 trillion a year). The Social Security Trust Fund is running dry, not because there are too many seniors, but because interest payments are consuming the federal budget that should be shoring it up.

There has been considerable discussion in recent years about reforming, modifying, or even abolishing the Federal Reserve. Proposals range from ending its independence, to integrating its functions into the U.S. Treasury Department, to dismantling it and returning monetary policy to direct congressional or Treasury oversight.

The Federal Reserve Board Abolition Act (H.R. 1846 and S. 869, 119th Congress, 2025-2026), introduced by Rep. Thomas Massie in the House and Sen. Mike Lee in the Senate on March 4, 2025, calls for abolishing the Fed’s Board of Governors and regional banks within one year of enactment, liquidating Fed assets and transferring net proceeds to the Treasury. It echoes earlier efforts like Ron Paul’s 1999 bill to “end the Fed”, but the odds of its passing are slim.

Less radical are proposals to curb the independence of the Federal Reserve. Former Fed governor Kevin Warsh is considered one of five finalists to take over as chairman after Jerome Powell. In a July 17 CNBC interview, he called for sweeping changes in how the central bank conducts business, and suggested a policy alliance with the Treasury Department.

Substantial precedent exists for that approach, both in the United States and abroad. In the 1930s and 1940s, before the Fed officially became “independent,” it worked with the federal government to fund the most productive period in our country’s history. More on that shortly.

The Federal Reserve’s independence is currently being challenged by political forces seeking to reshape its mandate. The Fed has not always been independent of Congress and the Treasury. Its independence was formalized only in 1951, with a Treasury-Federal Reserve Accord that was not a law but a policy agreement redefining the relationship of the parties. In the 1930s and 1940s, before the Fed officially became “independent,” it worked with the federal government to fund the most productive period in our country’s history. We can and should do that again.

In a Sept. 1 Substack post titled “Fed Faces Biggest Direct Challenge by a President Since JFK – and This Is a Good Thing,” UK Prof. Richard Werner shows that there is no evidence that more independent central banks deliver lower inflation. In fact, per his findings, central bank independence has no measurable impact on real economic performance, and greater central bank independence has resulted in lower economic growth.

This two-part series will probe the forces in play now to overhaul the Fed, and the feasibility of redirecting it to use its tools, including “quantitative easing,” not just to save the banks but to save the economy. Part I looks at a particularly flawed Fed policy — Interest on Reserves (IOR) — which burdens the budget, stifles liquidity, and subsidizes banks. Then it suggests ways that eliminating IOR and reining in the Fed’s independence could solve the Treasury’s interest burden altogether.

The U.S. national debt just passed $36 trillion, only four months after it passed $35 trillion and up $2 trillion for the year. Third quarter data is not yet available, but interest payments as a percent of tax receipts rose to 37.8% in the third quarter of 2024, the highest since 1996. That means interest is eating up over one-third of our tax revenues.

Total interest for the fiscal year hit $1.16 trillion, topping one trillion for the first time ever. That breaks down to $3 billion per day. For comparative purposes, an estimated $11 billion, or less than four days’ federal interest, would pay the median rent for all the homeless people in America for a year. The damage from Hurricane Helene in North Carolina alone is estimated at $53.6 billion, for which the state is expected to receive only $13.6 billion in federal support. The $40 billion funding gap is a sum we pay in less than two weeks in interest on the federal debt.

The current debt trajectory is clearly unsustainable, but what can be done about it? Raising taxes and trimming the budget can slow future growth of the debt, but they are unable to fix the underlying problem — a debt grown so massive that just the interest on it is crowding out expenditures on the public goods that are the primary purpose of government.

Borrowing Is Actually More Inflationary Than Printing

“Rather than collecting taxes from the wealthy,” wrote the New York Times Editorial Board in a July 7 opinion piece, “the government is paying the wealthy to borrow their money.”

Titled “America Is Living on Borrowed Money,” the editorial observes that over the next decade, according to the Congressional Budget Office (CBO), annual federal budget deficits will average around $2 trillion per year. By 2029, just the interest on the debt is projected to exceed the national defense budget, which currently eats up over half of the federal discretionary budget. In 2029, net interest on the debt is projected to total $1.07 trillion, while defense spending is projected at $1.04 trillion. By 2033, says the CBO, interest payments will reach a sum equal to 3.6 percent of the nation’s economic output.

On CNN March 14, Roger Altman, a former deputy Treasury secretary in the Clinton administration, said that American banks were on the verge of being nationalized:

What the authorities did over the weekend was absolutely profound. They guaranteed the deposits, all of them, at Silicon Valley Bank. What that really means … is that they have guaranteed the entire deposit base of the U.S. financial system. The entire deposit base. Why? Because you can’t guarantee all the deposits in Silicon Valley Bank and then the next day say to the depositors, say, at First Republic, sorry, yours aren’t guaranteed. Of course they are.

… So this is a breathtaking step which effectively nationalizes or federalizes the deposit base of the U.S. financial system.

The deposit base of the financial system has not actually been nationalized, but Congress is considering modifications to the FDIC insurance limit. Meanwhile, one state that does not face those problems is North Dakota, where its state-owned bank acts as a “mini-Fed” for the state. But first, a closer look at the issues.

Financial podcasts have been featuring ominous headlines lately along the lines of “Your Bank Can Legally Seize Your Money” and “Banks Can STEAL Your Money?! Here’s How!” The reference is to “bail-ins:” the provision under the 2010 Dodd-Frank Act allowing Systemically Important Financial Institutions (SIFIs, basically the biggest banks) to bail in or expropriate their creditors’ money in the event of insolvency. The problem is that depositors are classed as “creditors.” So how big is the risk to your deposit account? Part I of this two part article will review the bail-in issue. Part II will look at the derivatives risk that could trigger the next global financial crisis.

From Bailouts to Bail-Ins

The Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 states in its preamble that it will “protect the American taxpayer by ending bailouts.” But it does this under Title II by imposing the losses of insolvent financial companies on their common and preferred stockholders, debtholders, and other unsecured creditors, through an “orderly resolution” plan known as a “bail-in.”

The point of an orderly resolution under the Act is not to make depositors and other creditors whole. It is to prevent a systemwide disorderly resolution of the sort that followed the Lehman Brothers bankruptcy in 2008. Under the old liquidation rules, an insolvent bank was actually “liquidated”—its assets were sold off to repay depositors and creditors.

The Real Goal of Fed Policy: Breaking Inflation, the Middle Class or the Bubble Economy?

“There is no sense that inflation is coming down,” said Federal Reserve Chairman Jerome Powell at a November 2 press conference, — this despite eight months of aggressive interest rate hikes and “quantitative tightening.” On November 30, the stock market rallied when he said smaller interest rate increases are likely ahead and could start in December. But rates will still be increased, not cut. “By any standard, inflation remains much too high,” Powell said. “We will stay the course until the job is done.”

Fixing supply chains is of course beyond any central bank’s power. What the Fed can do is reduce spending levels, which would in turn exert downward pressure on prices. But this would be a mistaken response to shortages. It would answer a scarcity of goods by bringing about a scarcity of money. The effect would be to compound the hit to living standards that supply shocks already caused.

So why is the Fed forging ahead? Some pundits think Chairman Powell has something else up his sleeve.

It may be heresy to those who think the Fed is all-powerful, but the honest answer is that raising interest rates wouldn’t put out the fire. Short of throwing millions of people out of work in a recession, higher rates wouldn’t bring supply and demand back into balance, a necessary condition for price stability.

The Fed (and those who are clamoring for the Fed to raise rates immediately) have misdiagnosed the problem with the economy and are demanding the wrong kind of medicine. …

Prices are going up because crucial inputs—labor, electronics, energy, housing, transportation—are in short supply. Normally, the way to solve this imbalance would be to give workers and businesses incentives to increase their supply. …

The Fed has been assigned the job of fixing this. Unfortunately, the Fed doesn’t have the tools to do it. Monetary policy works (in theory) by tweaking demand, but it has no direct impact on supply.

The Fed has options for countering the record inflation the U.S. is facing that are more productive and less risky than raising interest rates.

The Federal Reserve is caught between a rock and a hard place. Inflation grew by 6.8% in November, the fastest in 40 years, a trend the Fed has now acknowledged is not “transitory.” The conventional theory is that inflation is due to too much money chasing too few goods, so the Fed is under heavy pressure to “tighten” or shrink the money supply. Its conventional tools for this purpose are to reduce asset purchases and raise interest rates. But corporate debt has risen by $1.3 trillion just since early 2020; so if the Fed raises rates, a massive wave of defaults is likely to result. According to financial advisor Graham Summers in an article titled “The Fed Is About to Start Playing with Matches Next to a $30 Trillion Debt Bomb,” the stock market could collapse by as much as 50%.

Whether the U.S. should have its own central bank digital currency (CBDC) is hotly debated. Several countries, including China, already have CBDCs in operation; but the U.S. Federal Reserve is proceeding with caution. Prof. Saule Omarova, President Biden’s nominee for Comptroller of the Currency, is in favor of a CBDC and has made a strong case for it; but many conservative commentators are opposed, and her nomination remains in doubt.

A self-funding national infrastructure bank modeled on the “American System” of Alexander Hamilton, Abraham Lincoln, and Franklin D. Roosevelt would help solve not one but two of the country’s biggest problems.

Millions of Americans have joined the ranks of the unemployed, and government relief checks and savings are running out; meanwhile, the country still needs trillions of dollars in infrastructure. Putting the unemployed to work on those infrastructure projects seems an obvious solution, especially given that the $600 or $700 stimulus checks Congress is planning on issuing will do little to address the growing crisis. Various plans for solving the infrastructure crisis involving public-private partnerships have been proposed, but they’ll invariably result in private investors reaping the profits while the public bears the costs and liabilities. We have relied for too long on private, often global, capital, while the Chinese run circles around us building infrastructure with credit simply created on the books of their government-owned banks. Continue reading →

The Fed’s policy tools – interest rate manipulation, quantitative easing, and “Special Purpose Vehicles” – have all failed to revive local economies suffering from government-mandated shutdowns. The Fed must rely on private banks to inject credit into Main Street, and private banks are currently unable or unwilling to do it. The tools the Fed actually needs are public banks, which could and would do the job.

On November 20, US Treasury Secretary Steven Mnuchin informed Federal Reserve Chairman Jerome Powell that he would not extend five of the Special Purpose Vehicles (SPVs) set up last spring to bail out bondholders, and that he wanted the $455 billion in taxpayer money back that the Treasury had sent to the Fed to capitalize these SPVs. The next day , Powell replied that he thought it was too soon – the SPVs still served a purpose – but he agreed to return the funds. Both had good grounds for their moves, but as Wolf Richter wrote on WolfStreet.com, “You’d think something earth-shattering happened based on the media hullabaloo that ensued.” Continue reading →

BlackRock is a global financial giant with customers in 100 countries and its tentacles in major asset classes all over the world; and it now manages the spigots to trillions of bailout dollars from the Federal Reserve. The fate of a large portion of the country’s corporations has been put in the hands of a megalithic private entity with the private capitalist mandate to make as much money as possible for its owners and investors; and that is what it has proceeded to do.

To most people, if they are familiar with it at all, BlackRock is an asset manager that helps pension funds and retirees manage their savings through “passive” investments that track the stock market. But working behind the scenes, it is much more than that. BlackRock has been called “the most powerful institution in the financial system,” “the most powerful company in the world” and the “secret power.” It is the world’s largest asset manager and “shadow bank,” larger than the world’s largest bank (which is in China), with over $7 trillion in assets under direct management and another $20 trillion managed through its Aladdin risk-monitoring software. BlackRock has also been called “the fourth branch of government” and “almost a shadow government”, but no part of it actually belongs to the government. Despite its size and global power, BlackRock is not even regulated as a “Systemically Important Financial Institution” under the Dodd-Frank Act, thanks to pressure from its CEO Larry Fink, who has long had “cozy” relationships with government officials. Continue reading →

Insolvent Wall Street banks have been quietly bailed out again. Banks made risk-free by the government should be public utilities.

When the Dodd Frank Act was passed in 2010, President Obama triumphantly declared, “No more bailouts!” But what the Act actually said was that the next time the banks failed, they would be subject to “bail ins” – the funds of their creditors, including their large depositors, would be tapped to cover their bad loans.

Many economists in the US and Europe argued that the next time the banks failed, they should be nationalized – taken over by the government as public utilities. But that opportunity was lost when, in September 2019 and again in March 2020, Wall Street banks were quietly bailed out from a liquidity crisis in the repo market that could otherwise have bankrupted them. There was no bail-in of private funds, no heated congressional debate, and no public vote. It was all done unilaterally by unelected bureaucrats at the Federal Reserve.

“The justification of private profit,” said President Franklin Roosevelt in a 1938 address, “is private risk.” Banking has now been made virtually risk-free, backed by the full faith and credit of the United States and its people. The American people are therefore entitled to share in the benefits and the profits. Banking needs to be made a public utility. Continue reading →

Congress seems to be at war with the states. Only $150 billion of its nearly $3 trillion coronavirus relief package – a mere 5% – has been allocated to the 50 states; and they are not allowed to use it where they need it most, to plug the holes in their budgets caused by the mandatory shutdown. On April 22, Senate Majority Leader Mitch McConnell said he was opposed to additional federal aid to the states, and that his preference was to allow states to go bankrupt.

No such threat looms over the banks, which have made out extremely well in this crisis. The Federal Reserve has dropped interest rates to 0.25%, eliminated reserve requirements, and relaxed capital requirements. Banks can now borrow effectively for free, without restrictions on the money’s use. Following the playbook of the 2008-09 bailout, they can make the funds available to their Wall Street cronies to buy up distressed Main Street assets at fire sale prices, while continuing to lend to credit cardholders at 21%.

If there is a silver lining to all this, it is that the Fed’s relaxed liquidity rules have made it easier for state and local governments to set up their own publicly-owned banks, something they should do post haste to take advantage of the Fed’s very generous new accommodations for banks. These public banks can then lend to local businesses, municipal agencies, and local citizens at substantially reduced rates while replenishing the local government’s coffers, recharging the Main Street economy and the government’s revenue base. Continue reading →

1176. 10-22-23, 10:45 am, speaker, The Weston A. Price Foundation’s 23rd Annual Conference, Kansas City, Missouri.

1175. 10-19-23, The Final Banking Solution, with Simon Thorpe and Colin Maxwell on The Vinny Eastwood Show, YouTube, Australia.

1174. 8-22-23, 10 am, Claremont, CA, Cobb Institute Center for Process, power point presentation: “Restoring Prosperity with a Financial Transaction Tax and Publicly Owned Banks.“ Zoom link is here.

1173. 6-15-23, NIB Zoom town hall, National Infrastructure Bank Coalition.

1172. 5-22-23: Radio interview, 9:30 am est, The Power Hour.

1171. 5-17-23: TV interview, CGTN America, Global Business: “Banking industry in hot seat during Congressional hearings.”

1170. Apr 27, National Infrastructure Bank Coalition webinar, “How to Build the Nation: National Banking vs. Privatization”

1160. 3-16-23, 5 pm pst, National Infrastructure Bank Coalition Town Hall, “Restructuring the American Workforce in a Time of Financial and Economic Turbulence.”

1156. 2-25-23, 15:00-17:00 GMT (Ireland), Think Local Conference 2023, Panel 3 – Money & Economics – New Paradigms

1155. 2-16-23, 5 pm pst, National Infrastructure Bank Coalition, “Washington, Hamilton, Lincoln: National Banking and the Economic Demands of Today’s Crisis,” NIB Zoom Town Hall

1130. Mar. 31, Power Point presentation on youtube, Universidad Nacional de Colombia, Invita: Debates Ensayos de Economia Coordina: Guillermo Maya — Profesor adscrito al Departamento de Economia

1115. Feb. 23, 7 pm est, Eco Justice Collaborative Webinar, “Why the Crises We Face Make Financial Reform Essential,” Religious Society of Friends, Philadelphia

1114. Feb. 17, 11 am, Steff Overbeck, Pod of Gold radio interview

1113. Feb. 18, radio interview, Phil Mikan, wlis1420

1112. Feb. 16, National Infrastructure Bank Coalition Presidents’ Day Webinar 2021 – “National Infrastructure Bank: Standing on the Shoulders of Giants”

1111. Feb. 6, radio interview, Sylvia Richardson, Latin Waves

1097. Oct. 26, Phil Mikan Show, WLIS/WMRD Radio, Conn., pre-recorded for Friday at 10 est or Saturday at 9-11 est

1096. Oct. 22, 1:15 pm EST, power point presentation, “Public Banking, Modern Monetary Theory (MMT) and the National Debt,” Carolina Hills Community, Chapel Hill, NC

1088. July 15, 6 pm EST, Connecticut Public Banking Town Hall, livestream here

1087. July 13, Webinar, Center for Global Justice, “Why Public Banking Needs to Be Run as a Public Utility,” San Miguel de Allende, Mexico, 11am-1pm PDT

1086. Interview with Susan Johnson on public banking for Connecticut, WILI’s Let’s Talk About It Show, 5 pm EST

1044. Nov. 12, interview in New York with Max Keiser, Keiser Report, “Repo Markets and UBI”

1043. Nov. 6, 5 pm EST, The CivicLab Show with Tom Tresser, live@www.facebook.com/tomtree

1042. Oct. 23, 11:30 am-1:30 pm, luncheon presentation on public banking, League of Women Voters of San Diego, Tom Ham’s Lighthouse Restaurant, 2150 Harbor Island Dr., San Diego

1041. Oct. 22, Presentation on public banking, DSA San Diego, Unite Here Union Hall, 2436 Market Street, San Diego, 6-7:30 pm.

1006. Oct. 22, speaker with Gar Alperovitz at Praxis Peace Institute, “Changing the System: California’s Strategic Role in National Strategic Change,” Sonoma, CA, 276 E. Napa St, Sonoma. 7:00 pm.

1005. Oct 19-21, Bioneers Conference, panelist on Oct 20, 2:45 pm, Marin Center, San Rafael, CA.997.

999. Oct. 7, panel, Americans for Democratic Action of Southern California Annual Garden Party, 2-5:30 pm, Santa Monica, CA

998. Oct. 4, 7:30 pm, Living Economy Salon, panelist, Public Bank LA: “Solutions for Social and Environmental Justice”, 3110 Main St., Annex Building C 2nd Floor, Santa Monica, CA 90405

997. Oct. 3, interview on Unmediated, podcast of Reader Magazine, episode title: Making Money The Public’s Slave (The Public Banking Solution), 10 a.m. PT

Regime Change at the Fed: From Big Bank Bailouts to Local Productivity

Image by ScheerPost.

On January 30, when former Federal Reserve board member Kevin Warsh was nominated by President Trump as the central bank’s next chair, markets sold off and gold and silver plunged. Investors were positioned for a “dove,” someone inclined to cut rates aggressively and keep money loose; and Warsh has a long-standing reputation as a “hawk.”

So wrote Michael Nicoletos in an article titled “Everyone Is Focusing on the Wrong Thing.” But Nicoletos and some other commentators are seeing something else on the horizon – a rebalancing of the banking system through an overhaul of the Federal Reserve itself. In recent months, noted Nicoletos, Warsh has argued that the central bank’s “bloated balance sheet” has made borrowing “too easy” for Wall Street, while leaving “credit on Main Street too tight.” That contrast — abundant liquidity for the largest financial institutions, scarcity for the communities that actually generate economic activity — is a structural flaw that has unbalanced the American economy.

Continue reading →Filed under: Ellen Brown Articles/Commentary | Tagged: Bank of North Dakota, community banks, economics, economy, Federal Reserve, FINANCE, Financial Regulation, Kevin Warsh, money, NATIONAL INFRASTRUCTURE BANK, politics, Public Banking, quantitative easing, Scott Bessent | 3 Comments »